Donald Trump’s top economic advisor claims the President has weaponised tariffs to ‘persuade’ other nations…

India follows the Neo-Liberal Monetary Norms: Contracting the space for financial inclusion in her economy Sunanda Sen and Zico Dasgupta

“Apprehensions by India and other countries of possible excesses in capital inflows and the inflationary impacts led them stiffen the domestic interest rates. The Fed, however has reversed its policy to meet domestic inflation by pitching the US Fed interest rate high. India’s response, as has been the case in other developing countries, was to follow suit, in order to avoid capital flights from the country. In both situations it was one of rising and high interest rates, periodically adjusted to take care of the on-going inflation.”

There have been significant changes in India’s financial regime since the early years of her independence when the majority of banks were nationalised in 1969, enabling the central bank to be in a position to administer interest rates and to fix 40% of deposits as directed priority credit to the deprived sections. Both were dissipated by the extensive economic reforms aiming to achieve financial efficiency.

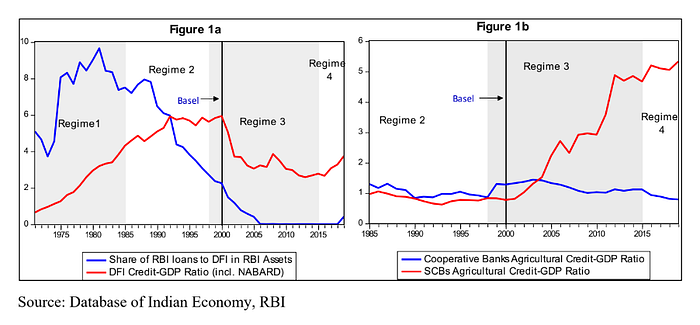

While implementing the major reforms as above, policies in India relied on the monetarist tool of inflation targeting, based initially on control over money supply and later, on the bank rate set by the central bank. We present here a tabulation of the successive monetary policy regimes in India, charting out the route taken by policies to replace developmental banking by what came up as profitability and stability of the financial sector. Regime 1 covers the years of developmental banking, which started when banks were nationalized in 1969. Financial inclusion was attempted at by setting credit targets for public sector banks at 40 percent of bank deposits and disbursing concessional loans to development financial institutions (DFIs). The DFIs were to provide concessional credit to the cooperative and regional rural banks, which remain the key agency of credit disbursement to households. In essence, the credit disbursement (asset side) of DFIs, cooperative and regional rural banks was all backed by RBI’s concessional credit (liability side) facilities. The regime witnessed the initiation of universal banking which allowed banks enter the security markets and also capital adequacy of banks, at 4 per cent, which later went up with Basel norms.

Regime II started in 1985/86 with inflation targeting as a major tool of policy. Other changes in policies include an end to expansionary financing of fiscal deficits by the central bank; which was considered inflationary. Henceforth the central bank had to sell bonds in the market for such financing.

However, with strong inflationary pressures, which to some extent was fueled by rising agricultural terms of trade, a cost push inflation was triggered, thereby squeezing industrial demand.

Situations as above led to a shift in policy stance during Regime II, which started relying on quantity of money supply as the major tool for inflation targeting. Above turned out, as held in post-Keynesian notion of endogenous money, as a poor substitute of credit in circulation. The failure has led the policy makers to revert in Regime III by relying on the policy rate of the central bank as the other tool for inflation targeting under monetarism. This continues at present.

Let us observe, in these changes the different stages of the implicit denials to financial inclusions. While the 40% limit for priority credit remained, permission was given to banks to freely charge interest rates on loans above Rs 0.2 millions, thus removing the cap so long specified by the central banks on such small loans. There also came up a major drive to change the functioning of the development banks in the country, which so far were providing concessional long term credit to projects on basis of “credit-worth judged by purpose” instead of the “credit-worthiness of the borrower”. The method was far more inclusive than the practice of the World Bank which defined financial inclusion by the role of banks in deposit-creation. Changes were now introduced by turning the development banks as regular profitmaking commercial banks. This was a big blow to the sources of developmental finance from the banking sector. Simultaneously the central bank’s responsibilities to the development banks was brought to an end. All these signified an end to the inclusivity of finance — all to achieve an “efficient” banking industry, as advocated in neo-liberal theory.

It can further be observed that the distribution of the priority credit, while continuing at 40% of bank deposits, remains grossly unequal. To look at Agriculture, which provides the mainstay of nearly 70% of India’s population, the share is a fair 18% of the priority credit. However, of this, the marginal farmers (land holdings not more than 1 to 2 hectors), can avail loans only up to Rs 0.2 mn — contrasting the Rs 500mn limit as maximum credit to medium enterprises under the category of Micro, Small and Medium enterprises (MSMEs). The latter have a share of 7.5% in priority credit. A similar dichotomy exists in providing priority sector loans up to Rs 3.5mn to help ‘low cost’ housing at cheaper rates in metropolitan cities. Concerns over possible defaults, continue to provide inclinations to screen the credit-worth of each loans, much to the insistence of the banking lobby in alliance to the state. We provide below two charts which reflect the much-diminished credit flows from the DFIs and the cooperative banks, supported by the former. As mentioned above these institutions remain the key agency of credit disbursement to households in rural areas.

Financial inclusion in India faced further challenges since the capital adequacy norms (CAR) were instituted by the Bank of International Settlements (BIS) in 1988. Banks in India today, as in most countries, are required to maintain equities, as assets in their portfolios, at the specified ratio of 9% of their risk-weighted assets under Base III. Successive increases in the CAR since its inception in 1988 has been hitting financial inclusion, especially by instituting the itemized Tier-wise risk assessment provided in the Basel norm II. As of now, while assets held by banks as Tier 1 are generally credit-worthy with little risk-weight or none, those in next Tier include potential risks which require additional equities to maintain the stipulated CAR. The differentiated risks on loans to different categories of bank clients made it extremely difficult for the poor and marginalized to get credit from banks.

As pointed out above, policy rates of the central bank are currently considered the major tool of inflation targeting. In the meantime, US Fed has launched the Quantitative Expansions (QE), since 2003, by injecting liquidity in their domestic market in a bid to revive the post- crisis US economy. The impact in the US credit market included sharp declines in domestic interest rates to levels approaching zero. Apprehensions by India and other countries of possible excesses in capital inflows and the inflationary impacts led them stiffen the domestic interest rates. The Fed, however has reversed its policy to meet domestic inflation by pitching the US Fed interest rate high. India’s response, as has been the case in other developing countries, was to follow suit, in order to avoid capital flights from the country. In both situations it was one of rising and high interest rates, periodically adjusted to take care of the on-going inflation.

Moves as above in Indian monetary policy indicate the abandoning of goals: both for autonomy in setting policies as well as for financial inclusion. The pattern reflects a subordinated status of India and the rest of the periphery, failing to have autonomy over domestic economic policies.

(This article was originally published in Monetary Policy Institute Blog on June 4, 2023)