Donald Trump’s top economic advisor claims the President has weaponised tariffs to ‘persuade’ other nations…

China’s Trade with other Asian countries C. P. Chandrasekhar and Jayati Ghosh

Just before the Global Financial Crisis more than a decade ago, China had emerged as the most significant trading partner for a majority of the world’s economies. Since then, it has had even more significant impacts on global exports and imports. This is especially true for developing countries, particularly those in developing Asia. (In the discussion that follows, only merchandise trade is considered.)

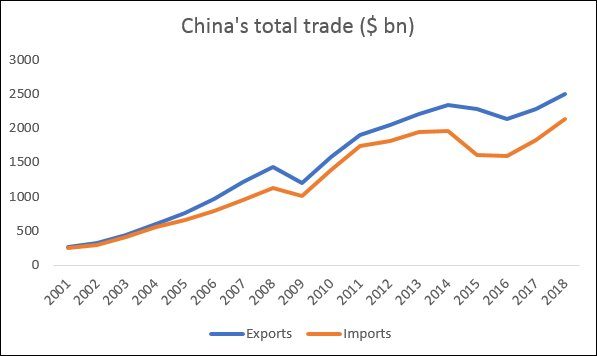

But these effects are now more complex. China’s now legendary trade surpluses began showing shortly after its entry into the WTO on 31 December 2001. As Figure 1 shows, exports increased rapidly until 2008, and also recovered fairly quickly after the Great Recession, growing at a similar or only slightly slower pace until 2014. Imports also grew rapidly, but less sharply than exports, so that the trade balance kept increasing. The trade surplus crossed $100 billion by 2005, tripled by 2008 to nearly $300 billion, and recovered after the fall of 2009 to reach nearly $680 billion by 2013. Since then, however, trade surpluses have been falling, although they still remain very large in absolute values.

Figure 1: China’s exports increased faster than imports after 2004

Source for all figures: IMF Direction of Trade Statistics.

Despite these large trade surpluses, China’s voracious demand for imports to fuel its processing exports operated as an engine of growth for developing countries, creating significant increases in demand for raw materials, energy and other intermediates. This created the desirable combination of improved export volumes and better terms of trade for many primary commodity exporters, and drew many developing economies into manufacturing value chains centred around China for purposes of ultimate export to advanced economies.

This process was especially evident in the economies of developing Asia. Figure 2 shows that trade with the rest of emerging and developing Asia, while growing rapidly, was mostly balanced until 2011, with small deficits for China until 2007 and small surpluses until 2011. Thereafter imports were stagnant for some years and then increased, even as exports kept growing. This created significant trade surpluses for China with the region, reaching around $130 billion in 2015.

Figure 2: Trade surpluses with developing Asia ballooned after 2011

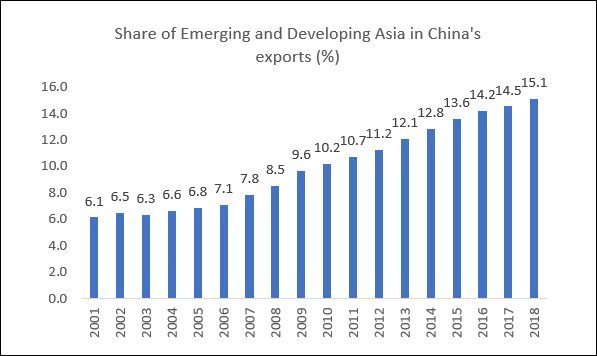

The dramatic growth of China’s exports to Asia even exceeded the pace of aggregate exports, so that the region’s share of China’s total exports doubled in the decade after the global financial crisis (Figure 3). This market is likely to become even more significant for China in future, with lagging demand in the North – and the exports are increasingly not only of manufactured consumer goods, but of the high technology goods that are at the forefront of China’s current growth strategy.

A closer consideration of specific countries in the region in Figure 4 reveals a mixed picture within this overall pattern of growing trade surpluses of China. Of the seven major Asian economies considered here, China has had persistent deficits only with Malaysia, which has generally exported high technology goods to China. However, such deficits also declined substantially between 2011 and 2015, and increased slightly thereafter but in 2018 still remained well below the level of 2011. With Thailand as well, China’s trade deficits have narrowed over the years, while the earlier deficit with the Philippines has moved to substantial surplus. Indonesia, Bangladesh, Vietnam and India all show trends of increasing surpluses, to varying degrees.

Figure 3: Developing Asia became much more important as a market for China’s exports

Figure 4: Trade surpluses have increased with some of the larger economies in the region

The biggest increase is in the trade surplus with India – a nearly threefold increase in the period between 2010 and 2018. Not only has China’s trade surplus with India grown, but the pattern indicates growing imbalance, as India exports mainly raw material like iron ore and processed agricultural goods, in return for receiving manufactured goods including a growing component of high technology items, from China. This means that this pattern of trade encourages increasing returns activities in China while Indian exports still reflect less technology-intensive goods that do not generate dynamic returns to scale.

The macroeconomic implications of this pattern may be just as significant as the developmental impact. For China, the Asian region is becoming increasingly important as a growing market for a wide range of its exports. For the rest of the countries in the region, however, on the whole the trade stimulus from China is negative, since the trade imbalance leads to a leakage of effective demand through imports. Moreover, since 2011, Chinese imports from developing and emerging Asia have been largely stagnant, barring a small increase in 2018.

This suggests that ongoing patterns of trade between China and the rest of developing Asia are likely to have significant effects on future growth and development in the region. And since this is still the most “dynamic” economic region in the world, that will have effects on international trade as well.

(This article was originally published in the Business Line on April 23, 2019)