Liberal opinion holds that the international monetary and financial system is a device for promoting…

Shadow Cast by the Rupee

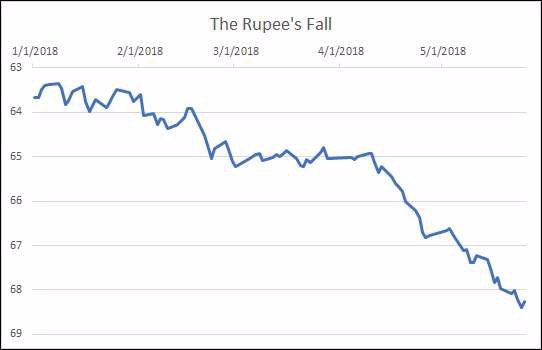

The rupee, which has been sliding in value for some time, has depreciated sharply in recent weeks, giving some cause for concern. The depreciation is largely against the rising dollar, relative to which its value has fallen by more than 7.5 per cent since the beginning of the year. The RBI’s reference rate which stood at Rs. 63.4 to the dollar on 5 January 2018 had touched Rs. 68.4 to the dollar by 24 May 2018 (See Chart). Depreciation relative to other major currencies like the British pound, the euro and the yen, has been much less. Yet, the fall vis-à-vis the dollar is of significance, especially since much of India’s trade and of its foreign debt is denominated in dollars.

Discussions on the rupee’s decline, which is projected to continue, focus on its proximate determinants. Prominent among these is the rise in the current account deficit on India’s balance of payments intensified by the recent sharp rise in the international price of oil. The current account deficit rose from $41.6 billion in 2016 to $73.3 billion in 2017. Further, the $23.2 billion deficit recorded in the last quarter of 2017 was significantly higher than that recorded in the previous July to September quarter ($14.4 billion) and in the last quarter of the previous year ($15.5 billion). The effects of this net outflow of foreign currency were enhanced by the retreat of investors because of rising interest rates in the advanced countries and the still hesitant recovery from the global recession. There was a net outflow of portfolio investments totaling $8.44 billion in the period starting 1 January to 25 May, 2018, with $7.95 billion flowing out in the first 25 days of May alone. Since some of these trends are not triggered by developments internal to India, the problem is seen not being India-specific, especially since they correspond to trends in emerging markets across the world, with matters being far worse in countries like Turkey and Argentina.

While these proximate explanations are indeed valid, the emphasis on them implicitly underplays what the tendency really reflects. Periodic bouts of rupee depreciation that sometimes even trigger panic are symptoms of India being a bubble economy. There are many features that warrant it being characterized as one. The first, and most obvious, is the fact that the purported success of liberalizing ‘reform’ lies not in the fact that India has been transformed (as intended) into an internationally competitive manufactured-exports-driven economy, but in its emergence as a favoured destination for international financial investors. The resulting large capital inflows have had a number of effects, all of which together define the bubble on which economic growth rides.

The inflows resulted in a medium-term spike in stock market values accompanied by significant volatility, with stock market valuations of many companies now at levels not warranted by potential earnings. Moreover, flows into debt markets have meant that India’s bond market which was earlier largely restricted to government bonds, is now seeing much activity in the corporate segment adding to the exposure to foreign debt of firms looking to benefit from low interest rates abroad. Since money borrowed at low interest rates in the advanced economies finances a large part of the foreign financial investment and since borrowing by Indian corporates is at low interest rates, the level of capital inflows is extremely sensitive to the interest rate in the developed countries. If because of changed circumstances in the source countries interest rates there were to rise, new flows would dry up and investors may choose to book profits and exit. This could not only unwind equity and debt markets, but also but also weaken the currency, making depreciation a reflection of the speculative investments that preceded the tendency.

Large inflows of foreign capital, by enhancing liquidity in the system, also trigger a credit boom with increased lending to the private sector (both households and firms). It is such lending that spurs demand and drives domestic market growth. Since debt financed consumption and investment in this scenario is driven by the pressure exerted by excess liquidity on banks to increase lending, the potential that agents who would not be able to service their debts would be drawn into the universe of borrowers is high. This increases the probability of default which, given the credit boom, can lead to systemic fragility. And such fragility can intensify the capital flight that generates exchange rate volatility.

Occurring in a context of import liberalization the demand fuelled by debt is likely to be more import intensive than would have otherwise been the case. Since liberalization in instances like India’s does not substantially enhance exports, the import intensive consumption and investment that accompanies capital inflows generates a third source of potential pressure on the rupee in the form of a widening current account deficit. If the foreign exchange outflow on account of imports of goods and services and other payments to non-residents exceeds inflows from exports of good and services and remittances, the deficit even if financed by capital inflows sends out signals that the currency is vulnerable. A country that cannot earn the foreign exchange needed to finance its current needs and must borrow to meet them is vulnerable to balance of payments difficulties and cannot sustain the value of its currency. However, till recently this problem was not visible because low oil prices had depressed and kept low outflows on account of imports of goods. And when that was not true, capital inflows helped finance large deficits. That is changing now as oil prices have risen to $80 a barrel, breaching a number of “psychological barriers”. The reality that India is a country that is vulnerable on the balance of payments front is asserting itself.

In sum, liberalized trade and liberalized capital flows have substantially enhanced India’s vulnerability, of which periodic episodes of currency depreciation are a symptom. Ironically, this tendency has been concealed by the large capital inflows spurred by liberalisation and by the benefits India derived from low oil prices. Both those advantages are now under threat. So is the unsustainable growth that capital flows and liquidity infusion stimulated.

Moreover, currency depreciation has effects that enhance pre-existing vulnerability. One form that takes is inflation. If trade liberalization has increased dependence on imports for consumption and investment, depreciation by raising the rupee costs of imports would aggravate inflation. Since one of the factors underlying the depreciation is an increase in the prices of a universal intermediate like oil, the potential for inflation is much higher. Inasmuch as the proximate factors underlying the depreciation of the rupee also create an environment where the growth generated becomes unsustainable, the joint effect of those factors and depreciation is a tendency to stagflation, or slow growth combined with inflation.

Inflation also forces the central bank, to withdraw from the cheap money policies of the high liquidity years and raise interest rates. Since low interest rates are the only macroeconomic instrument, howsoever effective, acceptable to neoliberal policy makers committed to fiscal austerity, the situation is one where there are no means to pull the economy out of the stagflation that envelopes it.

There is one other development flowing from currency depreciation that can compound these difficulties. As noted earlier, an aspect of the surge in capital flows to markets like India is an increase in private foreign debt, as corporations seek to exploit the low interest rates prevailing in the developed countries and the greater freedom to borrow abroad that liberalization provides. Since large capital inflows make the domestic currency appear strong, much of this borrowing in foreign currency is not hedged for possible losses stemming from any currency depreciation. When depreciation actually occurs, however, the rupee costs of servicing foreign debt rises sharply. This is also the time when the stagflation afflicting the economy hurts corporate profits, making the burden of servicing foreign debt too much to bear. The distress sale of assets that follow bankruptcies results in asset price deflation that worsens the problem.

Depending on the intensity of these effects, the bubble can burst and the game of speculation can unravel. It is for this reason that this round of currency depreciation is likely to be scrutinized carefully. It could be the round in which the bubble economy becomes unsustainable.

(This article was originally published in the Frontline Print edition: June 22, 2018)